If there’s one thing successful PT owners have learned, it’s that the key to their goal and vision is to have a great understanding of their cash flows. If you want to be successful, you need to know where it comes from, where it’s going, how it’s handled, and how it’s spent. If you neglect your financials and DON’T manage your cash flow strictly, you can say goodbye to your business. In this episode, Eric Miller of Econologics shares with your host, Nathan Shields, the ten key characteristics that financially successful owners should have. After years of working with successful owners, Eric believes these characteristics are 100% legit. These key traits will set any owner up for success going forward.

—

Listen to the podcast here

The Top 10 Characteristics Of Financially Successful Owners With Eric Miller Of Econologics

I’ve got a multi-time guest, frequent flyer, whatever you want to call it, everyone’s favorite financial advisor, Eric Miller of Econologics, talking about money. I always get excited about these episodes because we get to talk about money and what it takes to make more.

I hope we don’t bore people too much.

I’m excited. I hope that the audience gets excited, too.

It’s going to be good. We’re talking a little bit about the tactics, the tips and the tricks. It’s more of the meat in the bones of who you got to be, that identity, that you want to be successful with money. I’m stealing your thunder a little bit.

I love that you brought it up that way. You sent me a list of ten characteristics of top owners who achieve financial freedom. One of the purposes behind the podcast is to help owners generate more profit and freedom because many times and I learned this in the early stages of my clinic ownership is I had the money. Financially, I was doing okay but I didn’t have time. I didn’t have time to spend with my family, do the things that I wanted to do and that kind of stuff.

When you can generate a little bit more profit, then that can translate into personal freedom. I love to quote Will Humphreys. He said something like, “Profitability unlocks possibility.” When you can see the financial profit increase, then you have greater freedoms afforded to you and it’s valuable to recognize what you have to be in order to get some financial freedom?

You bet I will. I’m going to steal that from him. He should probably get that copyrighted because I like that.

When he said that, I was like, “Someone had to have said that before. It sounds classic.”

That’s true. “Profitability unlocks possibility.” It allows you to reach more because the derivation of profit means to expand. You can’t expand on debt forever. You have to expand on having profits as well. It is a key thing. That’s a good thing.

The headline of the document is, What Do You Need to Be. Let’s go with that. Tell us a little about when did you decide to start this Top 10 list and what inspired you to create it?

Eric Miller is helping PT owners become wealthy. Click To TweetThe benefit that I get is I get to talk to a lot of practice owners. I get to see the differences between the ones who are doing well financially and the ones who are struggling or you can see where it is the ones that are doing well. Here are some characteristics that I can impart upon the ones that are not doing well so they can see, “I need to change my identity a little bit because I’m not adopting that identity to be successful financially.” There’s a difference between being a practitioner. A lot of people understand that if I’m going to help someone with their mobility or to reduce their pain, I have to put on the hat of a physical therapist. I’ve got to be a physical therapist.

Your money in your business is totally different. You have to change the hat. It doesn’t mean you have to fake it. You may have to fake it until you make it in the beginning but you do have to make sure that this becomes part of you when you’re wearing that hat. You understand what the best owners are doing or have people around them that are doing when it comes to achieving financial freedom. That’s where that list came up and I started putting it together with, “These are all the things that I see.” Not every single one of the top owners does all these things super well but these are general characteristics that I see in most of them that are doing well. That’s where the list came from.

Let’s start with the first one. Let’s dissect this thing.

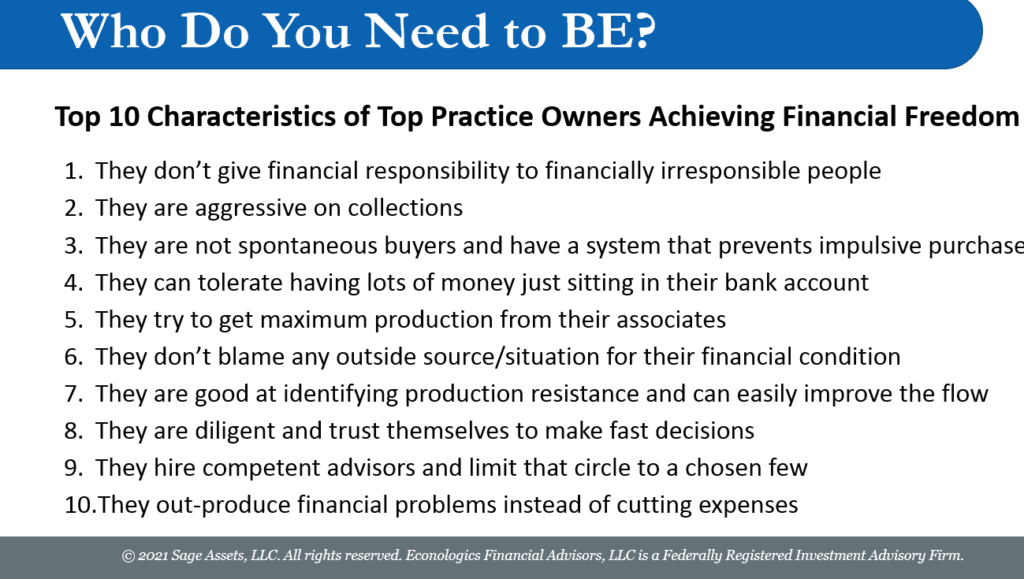

Number one, top practitioners don’t give financial responsibility to financially irresponsible people. It sounds pretty simple but I do think there’s a tendency sometimes that I’ve seen where owners have given the books or some part of the income line has given to people who are not responsible at all or they yo-yo.

They’re people who are always doing good, have personal problems, they’re doing good and they have more personal problems. If these people are in charge of your collections and getting money into the door, you’re going to struggle because money does not like that for whatever reason. That’s where that came from. Put them somewhere else in the organization but they can’t be on your money lines at all.

A lot of collections come across the front desk. You’re going to have to hold those people responsible at the front desk and sometimes above them, their supervisor could be a front office person who oversees the over-the-counter collections. It could be a collections person that oversees the transactions there as well. I lost money as an owner. In that regard, I didn’t take financial responsibility for tracking the money that came over the counter and that’s where I lost my money. I didn’t have a system in place. I didn’t take on the responsibility. I just expected them to collect, collect the copays and all that stuff but I didn’t have a system in place to track the collections and ensure that those over-the-counter collections matched up with my bank deposits.

That makes sense. That was a responsibility point that you had to get in place and you did.

When I finally took responsibility for it, I could look back on years of not having that system in place and losing thousands and thousands of dollars. The deposits showed the difference.

This isn’t just in the business, too. This could be in the household. You don’t want to give financially irresponsible people access to being able to spend whatever they want to. It’s a characteristic, in general, in life that will do you well if you do that. Aggressive on collections, it’s one of those things where you can’t sit back and hope the money comes in. You have to get aggressive on the collections. Here’s the thing.

Most practice owners don’t like to worry about the money side. They want to do the practitioner’s work. I get that the service that you deliver is valuable. You should get compensated for it. You have to make sure it’s done quickly and someone is aggressive on that. You definitely need a bulldog in that area. Someone will not take no for an answer or take all the excuses and the objections from the insurance companies. It’s a bulldog mentality, you just have to have that, either you have it or if you don’t have it, then you hire someone that does have it on the collection wise.

That adjective comes up often when I talk about good billers, not amongst my billers but other owners. They have a bulldog mentality. It’s funny. If my company is not getting paid, the right biller’s personality is such that they take it personally. They get mad when someone’s not paying, whether it’s a $20 copay or an insurance company that owes us $100 or $1,000. It doesn’t matter. They take it personally that these people are not paying. They owe this money and they’re not paying it. They get more upset about it than I do because I don’t have that bulldog mentality. I need someone like that to have that mentality that number one, is going to go after everything that’s owed to us. Number two, not be afraid to get on the phone and say, “You have a balance due. How are you going to pay for it now?” Also, not be afraid to have that conversation.

They can’t confront that. I’m like, “How much money are you giving away because you have people there that are afraid to ask for that?” It’s a lot sometimes.

A good question that Will Humphreys asks, now that he’s doing his billing and collections company is, “Are you 100% confident that you’re collecting everything that you build?”

It’s 100%. It’s not 90% or 95%. You have to go in with that attitude.

You have to have that mentality. That’s his question when you talk to these owners. I could say that for many years of my business ownership life, I would not be able to say that positively. Not until I finally got some systems in place, found the right person with the right mentality, was when I was able to finally say that for a few years of my business ownership. Number three.

They’re not spontaneous buyers and have a system that prevents impulsive purchases. I want people to have whatever they want to have. Certainly, I want to be able to have people practice owners that can go buy things when they want to. It’s impulsiveness. It’s the, “I have to have it now.” That’s where no one could put any discipline or, “I have to make it before I spend it,” kind of thing. The best donors have a purchase order system or something that is in the business that prevents purchases or there’s a manner that makes it difficult for money to leave the organization.

You find that a lot amongst PTA owners that they are impulsive buyers.

Maybe on the household side but not so much on the practice side because there’s not tons of equipment and everything that you needed to run up through PT practice like in other practices but I still see some of that. You have to have a system in place that makes it difficult for money to leave. I don’t notice it as much.

I tend to find that most PT owners are cheap. I don’t see a lot of them.

That’s Nathan Shields who said that. It wasn’t Eric Miller who said that.

Don't give financial responsibility to financially irresponsible people. Click To TweetI might need to copyright that. I don’t know if that’s what you want to share.

There’s some of that and honestly, something that they have to recognize is don’t be cheap. Be prudent but don’t be a miser. You’ve got to spend money sometimes. I will encourage people like, “You’ve got to spend money. Buy that $60 bottle of wine.” Act like someone who got money. Eventually, you will be someone that has money. That’s a fine line. You don’t want to spend all your money just because you think you deserve the highlight. There also has to be a production in that backside as well.

I tend towards that and maybe that’s because our profit margins aren’t the greatest. We have to be careful. At the same time, there’s a difference between the scarcity mindset and the abundance mindset. PT owners tend to go down that scarcity mindset a little too often. Maybe we lean towards that, personally. That’s what I see and there’s rarely a PT owner that’s in an abundance mindset like, “I could have as many new patients as I want if I find the right way, the avenue or the channel, whatever it is I need to tap into,” rather it’s more like, “I’m fighting for new patients versus this guy down the street over the smallest portion of people who are looking for PT.”

There is that mindset there that, “I’ve got to watch my dollars because I don’t know if I’m going to have enough patients coming in.” You’ve got to trust yourself and every area of your organization is working to bring money in.

Number four.

People look at this like, “I don’t understand what that means.” They can tolerate having lots of money sitting in their bank account. Some people see $20,000 in their bank account and they’ve got to spend it. It has to be spent. What I’ve seen the best owners do there is number one, assign money a purpose. It’s not sitting there for the sake of sitting there. It’s there for a purpose. It’s okay. “I can’t have a couple of $100 sitting in my business checking account. I don’t need to spend it on something. I can tolerate it being there,” and they’re more relaxed about that.

I was like, “I got all this money. What should I do with it? Should I do this? Should I do that?” They get totally nervous about the fact that they even have some. Maybe that’s because I’ve never seen it before. It’s like, “I don’t know what to do.” Relax and that’s where having a system of making sure you know that money is being channeled correctly to certain areas and if there’s a surplus there, great. You can take it, maybe use it for the improvement of the business to improve the value of the business. That’s where you should spend a lot of the money.

People don’t realize that if you hire a good coach or a good consultant, let’s say your profitability is at 9% and by working with someone, it gets up to 15%. It’s only a 6% increase but I’m like, “No, no.” That 6%, whatever that amount of earnings are, you’ve got to remember that the value of your business is based upon a multiple of your earnings, not just one. It could be as high as 6% or 7%. If you hire a good coach or consultant that gets your profitability up, that could be worth hundreds, if not millions of dollars. They have to be able to recognize that there’s an investment and an expense, and that needs to be recognized.

I’m glad you brought up that last bit. A lot of owners don’t recognize that when they’re bringing on the next PT, that’s not an expense. That’s an investment because this person can churn out multiples of their salary expense towards your bottom line. That’s an investment. It’s not lost money.

That builds the value of the business. That’s what an owner thinks because their owner mentality is working on enterprise value. A practitioner is only thinking of the cost. That’s where you have to separate out those two and have that owner mindset.

Based on this step alone, I have to reference people back to a previous episode that I did with you probably August 2020 or September 2020. We talked about the 5 or 6 different bank accounts that you should have to allocate money towards all the things that you might need as a business owner, as well as fund money and stuff that is allocated to be spent and not invested in the business. When you’re talking about having a lot of money in a bank account, it reminded me that we had this talk where people need to recognize they should have 5 or 6 different bank accounts to allocate the resources to different things and make that money work intentionally.

It’s in there for a reason, whether it’s acting as a backup in case there’s a shutdown, whether it’s for taxes or expansion, it should have a purpose for it first and foremost.

That reminds me of an experience that happened a couple of times, unfortunately, when my CPA called me in the middle of April 2021 and said, “You had a great year in 2020. You’re going to have to pay $80,000 in taxes. Are you ready to do that?” I’m like, “What?”

“No, I am not.”

If you haven’t set aside money for taxes and worked with your CPA over the course of the past year, set aside some money for taxes and have some communication with your CPA on a routine basis.

That’s something we have to hear more often than not.

Number five.

If you’ve got a PT, bring on, they’re worth a certain dollar amount of production and you’ve got to get maximum production out of them. They have a salary but it’s not just that, they have to get in return more than what their salary is going to cost. It’s got to be 4 to 5 times more if you’re going to be profitable. That means you’ve got to make sure that they’re scheduling people and asking for referrals. Get maximum production from your associate. You have to look at it like that. Some people aren’t comfortable with that.

I don’t think a lot of owners know exactly what stats they need to track in order to maximize productivity. We’ve shared statistics that are important to production on the show and in fact, maybe my last episode prior to this one was about maximizing production in getting patients to come in on an average of three times or closer to three times per week if you’re a regular outpatient orthopedic practice. Most owners don’t know what they need to do to maximize productivity in their clinics and that’s where they need to talk to somebody.

They need to reach out to their networks. They need to find a coach or consultant in the PT industry to let them know what exactly it is to do to increase productivity. They should be producing. The number that I’ve heard in the industry, Eric is, 3.5 to 4 times their salary having to be general to cover all of the states, a typical expectation for the productivity of a physical therapist.

Don't be cheap. Be prudent, but don't be a miser. Click To TweetThe 3.5 to 4 times their salary is probably minimum. I don’t know why some owners can’t do that. In my business, I have advisors and I expect them to do a certain level of production and they know that going in. It’s about care. It’s about getting someone to get a result but that usually represents if you’re doing a good job, then you should be getting production. Production should be occurring.

You said something valuable there that they know going in. Before you even hire them, they know what the production expectations are. That conversation doesn’t happen a lot when owners are talking to potential PT candidates that join their practice. They don’t have productivity expectation conversations and that’s where we do the PT a disservice. It’s to hire them, come back around and later and say, “You’re not producing like I expected you to.” That can be a slap in the face because you never laid out the expectations in the first place.

The person didn’t know what they were supposed to do in the first place and if they didn’t have those targets, then you can’t blame them for that.

That’s where they become disillusioned. At that point, they’re thinking, “That’s not what I signed up for. I thought you guys were different. You’re just running a PT mill here and you’re all about the money.” You should have had the conversation beforehand.

Anybody that says that you guys are all about the money, I take exception to that because they don’t see behind the scenes the stress, the late nights, the risk, and all the debt load that you have to carry as an owner, in some cases, it just means massive amounts of risk.

It’s an easy fallback for an employee to say something like that but at the same time, if you haven’t been clear about your expectations and how these things that we’re tracking, result in better patient care, lifestyle for you personally and an increase in salary for you and possible promotion. If you’re not making those connections with them, that’s what they’re going to easily fall back to, unfortunately, in some way for sure.

What’s next on this glorious list? I’m hoping people are like, “I’m doing some of this stuff.” They don’t blame any outside source situation for their financial condition. It’s the easiest thing to do, I hear this all the time, “I can’t find people. People are tough to find. Can’t find PTs. The economy is slowing down. Insurance isn’t paying me.” I’m like, “At some point of time, you’re going to have to say, ‘Stop.’” None of that is going to pay your expenses. It is not going to pay payroll. It’s not going to cover anything. It’s like, “I know that it’s fun to do and we all can sit there and have a bit session about it.” When I see someone that’s struggling financially, 99.9% of the time, it is never an external factor. It is an inside job.

I came across a quote from Brené Brown and it was something to the effect of, “Blame is the inverse of accountability.” If you find yourself blaming, then at some level, you are not being accountable to it.

Will Humphreys is going to take credit for that one too, isn’t he?

Next one.

You have to take responsibility for the funding. There’s something internally that you could do that would improve the financial condition of the business. Internally somewhere, it’s not working yet, you just have to spot where it is. That’s all. The best owners are super good at identifying production resistance and can easily improve the flow. Production resistance is when someone comes into your office, they get greeted and routed to wherever they need to go to get treated.

They get treated, go back, get rescheduled and money is collected. There’s a flow line in a business in a PT practice. The best owners are good at identifying where someone either isn’t applying a policy that they should, being defiant or not doing their job and able to spot it super quickly so they can improve that line. That’s the key. You’ve got to be able to observe what’s happening in the business.

When you say observe, you can watch people on the floor but also by observing your statistics if you’re tracking them properly, you can see resistance if the percentage of over-the-counter copays is not close to 100%. If it’s at 50%, then you’ve got some resistance at the front desk not being willing to confront the patients as they come in to accept the copay and talk to them appropriately. That could be an example of production resistance.

Whatever that is, there’s something that’s not optimum there. If you’re 100% practicing and you’re not setting the time aside to do executive work or to observe the practice, and do those things, you’re not going to spot that. The stats will give you an indicator but there is that point of making sure that you keep a pulse on the organization that way or have somebody that is looking at it. It’s like a casino in Vegas. They have the pit bosses, the people watching them and you have the guy in the sky watching them. Unfortunately, sometimes you need to have that accountability in the organization. Everybody’s watching each other.

If one of your productivity measures is to ensure that say, patients are coming at least two times per week for an orthopedic condition, it’s important for you to then observe in real-life situations how your providers are talking to their therapist and explaining out the plan of care. “If we’re going to get you better, you have to come for twelve visits.” That’s either 3 times a week for 6 weeks or 3 times a week for 4 weeks. Whatever you want to make for a plan of care, you have to come in for twelve visits, and they need to be having that conversation with the patient and you need to observe if that’s working well if it’s not and what they’re doing that you could give some advice to them. That’s production resistance as well.

What are the objections the patient gives? They’re like, “I don’t have the time.” You’ve got to have a handle on it. It’s training for the staff being able to handle objections. You could go through an organization. If you figured out how to handle every objection that someone gets somewhere in the organization, you’d probably double in size because you know how to handle what the objection would be. Handling objections is such a big deal. It’s like, “I don’t want to do it because of this.” “I got it. What about this?”

When you bring up production resistance, there’s a lot that, at least in the PT space, production resistance is an inability or an unwillingness to handle objections appropriately.

What’s good for the patient?

What’s best for the patient is usually what’s best for the business.

You know that. Why are you letting them off the hook?

Recognize that there's a difference between an investment and an expense. Click To TweetI love how you brought up identifying production resistance. It can happen at so many different levels within a PT clinic but there has to be an opportunity for you to number one, observe and assess. I recommend looking at statistics so you can get some objective data. It’s one thing to think, “There’s a problem over here but you can be certain if you have the data.”

You get dialed into where that happens in a PT practice. You can find out right there the conversation between the patient and the PT. It happens everywhere but you have to know that you’re working with somebody that knows a practice like yours too so they can help spot that for you. It’s definitely key. Number eight, they are diligent and trust themselves to make fast decisions. The best owners don’t suffer from analysis paralysis. Stop thinking so much and make a decision.

I don’t know about you but we’ve been an owner for many years. I’ve made bad decisions. Of course, we all have. One day, I had a coach tell me, “Eric, if you’re going to make a mistake, at least do it 180 miles an hour.” That always stuck with me, because it’s like, “Make fast decisions. You don’t have to be right 100% of the time, you don’t even have to be right 70% of the time. As long as you’re right 51% of the time, you’re going to be okay. You don’t need an A. You need to be right, more than often than you’re wrong to be successful in business.”

This isn’t for financial decisions. This can be applied to anything.

Everything. Definitely, trust yourself and make fast decisions. Be thoughtful and diligent but diligence doesn’t mean take ten weeks to figure something out. I’m sure you run into that.

All the time. It’s juxtaposed against number three, which is they are not spontaneous buyers. It’s not as if you’re saying, “Make a decision on A versus B now without looking at any of the data.” That’s not what you’re talking about.

Not at all. That’s impulsive. Impulsive is like there’s a compulsion to do something. It’s like, “I need to have that beer now.” That’s impulsive, whereas being diligent and making facts, “I see the data. The good outweighs the bad on that. I’m going to make the decision and go,” and not, “Let me talk to seven people and see what they say and go for all these other opinions.” It’s been one of those weeks where we run into people who get analysis paralysis and it’s maddening, especially on money. Money doesn’t like waiting. It likes speed. The faster you make decisions, the faster that money can come into your life. That’s Eric Miller. Tell Will Humphreys that he can’t steal that.

Take that, Will Humphreys. I’m one of those people who are slow decision-makers. My coach told me, “If someone asks you to make a decision now, tell him you got to sleep on it,” because I have to think about the different options and weigh out the pros and cons, whereas my wife is different. Will Humphreys’s partner is different. Sometimes they were a little frustrated with me and I know my wife gets frustrated with me. Give me a second, let me think about it. That’s okay. When it’s dragging on 2 to 3 weeks, and the team is waiting, “When are you going to make it? We’re waiting for the owner to make the decision.”

That starts affecting other people. They like confidence. I read somewhere that the best owners make fast decisions. Not impulsively like you’re talking about but they make quick decisions, recognizing that worst-case scenario if it’s a bad decision, there’s a plan B. You can make a U-turn, go back to the other option and all hell is not going to break loose. Make the decision. Find out that it’s the wrong decision quickly and then go where you got to go if it was a bad decision.

Being thoughtful and taking a day or two is not a bad thing. It’s when it draws out and you’re stuck in the maybe and you never make a decision. That’s where it gets destructive.

It starts affecting other people’s confidence in your ability as a leader at that time.

This one’s self-explanatory. I will tell you that the people that tried to do it themselves, I’ll let you know that the best owners do not adopt that viewpoint at all. They hire competent advisors and they have a circle of people that they trust and it’s not this huge circle of having seventeen different consultants and 54 different advisors that I’m going to go to. They keep it very close but they do hire them. They’re definitely not DIY people, Do-It-Yourselfers.

One hundred percent of my successful interviews on the show of owners who have done well, they are successful. One hundred percent have had some coach, consultant or mentor along the way. Even the ones that I thought, “This guy did it all himself,” after talking to him a little bit he’s like, “I did this or worked with this guy for some time or I’ve had a mentor over their years that was willing to give his time.” Inevitably, all of them have had some advisor, coach or consultant that has helped them be successful.

“I can’t imagine that you would want to do it on your own. I’m sure you could figure it out but you need a team to be able to make decisions, get the right data, have another perspective that maybe you don’t have.” That’s been extremely valuable. In helping owners, I’ve stopped people from selling their business when they were frustrated and burned out, I’m like, “Don’t do it now. Wait until you’re in a better frame of mind.” That paid off in millions and millions of dollars because they did end up selling what they did when they were in a much better frame of mind and their profitability, coincidentally, was higher because they were in a better frame of mind.

There is a cost to it when you don’t have people around you. The cost of consulting is peanuts when you look at it. They have to be competent, good and they have to give you good decisions, and areas to look at. If they’re good, the value of your business, especially in this industry where practices are selling anywhere between 6 to 8 multiples if you’re good practice. Think about that. I hire a coach for $20,000 that helped me improve my profitability by $100,000. That’s $600,000 of value that I added to my business.

You’re not exaggerating things.

That’s on the small side. You have to think about that. One guy hired a consultant and his profitability went from 9% to 20%. It’s an 11% increase and it wasn’t a small amount. It probably got him another $8 million to $9 million on his sale. You’ve got to recognize the value of a good consultant.

Physical therapists, honestly, have to recognize that they have zero business training most of the time. To think that you can simply hang your shingle out there, start a PT practice and it’d be an automatically successful business is naive.

There was no school. You can see in the financial curriculum that they’ve essentially omitted any real business training financial or personal financial training. They don’t teach that anymore. They didn’t when I was growing up. I never taught anything like that. They certainly don’t teach it in physical therapy school so you’ve got to learn that through the school of hard knocks or find someone that can help because you’re not going to learn any other way.

I’ve paid hundreds of thousands of dollars of tuition to the school of hard knocks, unfortunately, where I could have saved that money.

Blaming is the inverse of accountability. Click To TweetYou’re like an honorary member.

I’ve got my diploma.

Did you get a Doctorate from the school of hard knocks?

I spent enough money to earn it. I should have at least a certificate but I don’t and that money would have been well-served if I had hired a coach much earlier in my career.

That’s funny. I like that, too. I’ve got a Doctorate in the school of hard knocks.

I paid enough. I hope it’s a Doctorate.

Lastly, this applies especially in 2020 when I saw the best donors. They tried to outproduce the financial problems, instead of cutting expenses. We’re all going to be faced with circumstances that the first impulse is, “I’ve got to cut.” You have to recognize expenses when you’re having cashflow problems I’ve never seen anybody cut their expenses and achieve solvency.

The idea being, “Let’s cut our expenses to profitability,” doesn’t quite happen that way.

It goes against every Natural Law of Business it seems like. You have to figure out how I am going to outproduce this problem. How am I going to get more patients in the door? How am I going to do this to create more of an inflow of new people or correct something that is not happening, in the business that it should be so I can use that to solve the problem and not cut expenses?

I remember that distinctly from getting consulting that the last expense that you ever want to cut is your marketing. That’s maybe where we might naturally go towards it’s like, “Is this making me money?” It’s appropriate to assess the ROI on the marketing dollars spent but the last thing you need to do is shrink the budget if things are slowing down.

I rarely have ever seen someone cut their marketing budget and all of a sudden, they have an inflow of new patients coming in. The action of marketing, as long as it’s effective and the amount of outflow is going to help in some way, shape or form but cutting it is definitely not a good thing. Those are the ten things. I could probably come up with twenty. I don’t look at that. Imagine if someone was doing all those things, I would have a tough time thinking that they would be in a non-optimum financial condition.

When you list these ten things, do you see them in order of priority, necessarily or do you think some simply stand out more than others based on your experience?

I didn’t put them up as a priority on any one of them. Certainly, number one is a death knell to the organization. I certainly think that has a higher priority for sure, maybe number four. Number five, getting maximum production out of their associates is super important. Number two is important. Number six is important too because once you start blaming now, all of a sudden, you become an effect, and not the cause point. That’s more of a mindset thing. Number seven, you talked about that. You can handle a lot of problems. I didn’t put them in priority order but there are definitely things here that stand out more than others as being of senior importance.

It’s interesting because some of them are action items seemingly or could be afraid as action items and some of them are simply mindsets or belief systems if you will. I’m not going to give my cashflow over to someone who I can’t trust and with proper monitoring in place. It all fits number one. Number two, I want that person to have that mentality when it comes to collections. How do I hire for that?

Look at these things and inspect your own business. You can at least come up with some action plans of what to do to improve. All these things put together would increase someone’s production by 10% to 20%, almost immediately.

Easily. Any owner, whether they’re seasoned, successful or not, could look at a list like that, find some weak points and say, “How can we improve it in this, at least?” As I’m looking at it, I’m thinking, “That could be better. Take those things, and maybe prioritize them yourselves like, ‘Which of these things will generate more profit for me if I work on it now?’” Start there and work down the others.

Whatever sticks out because everyone’s going to look at that and say, “I can confront that.” Do that then. Even one. Do something. Don’t sit back and accept the situation as it is.

Thanks for sharing. Do you have that posted somewhere like on your website? Do people have to take a screenshot of what I threw up here?

I’ll make a download of that at some point in time so we’ll put it on as a download. I haven’t quite done that yet.

For those who are reading, they can go to the website, PTOClub.com and go to Eric’s episode here with me. This is August 2021 and finds it as a potential download there, too.

Money does not like waiting. It likes speed. Click To TweetI’m going to have the data for sure. I want them to have the data.

If people wanted to talk to you directly about stuff like this, how do they do that?

They can email me at [email protected]. I’m always open to someone communicating with me. They can go to our website EconologicsFinancialAdvisors.com, or go to Econologics.com. We have assessments. They can download a vast array of material that pertains to them as practice owners and success with their finances. We have a lot of downloads and financial success guides for private practice physical therapists. We try to cater to what you guys need.

Would you say you have a plethora of things?

You’ve got to stop using these big words, Nate. That Alaskan education up there is coming full bore. I can see it.

My family watched Three Amigos so that’s where that comes from. Thanks for your time. It’s always great to have you on the show and before we even pushed record, we already talked about a couple more topics that we need to get together on. Hopefully, those who are reading and look forward to those in the near future. We’re potentially talking about an expansion checklist like when to expand, how to expand and what indicators you want to follow in order to consider expansion. The other being, a partnership. If you have a favorite employee that wants to partner or do something, expand with you and that kind of thing, and what to consider when bringing on a partner.

Those are key because I get a lot of practice owners that are scared to death about expanding. It seems to be one of those fears of, “I don’t trust that I’ll have enough resources to be able to expand.” I get it. You have to have the mindset though that you’re going to expand because you’re never going to go sideways. You’re either going up or you’re going down. That will be an exciting one. We’ll definitely dig into that one.

That’d be great. Thanks for your time. I appreciate it, Eric.

It’s good to see you.

We’ll catch you next time.

Important Links

- Econologics

- Will Humphreys

- Episode – Re-Establishing Your Financial Foundation: Ramping Up After Covid-19 With Eric Miller

- Episode – 8 Key Steps to Success as a PT Clinic Owner

- [email protected]

About Eric Miller

Eric Miller has been in the financial planning industry for over 20 years. He’s a co-owner of Econologics Financial Advisors – awarded an Inc. 5000 honoree for 2019. As the Chief Financial Advisor for the firm, Eric has had the good fortune to have over 10,000 financial conversations with private practice owners in various healthcare industry and helped guide them into a more optimum financial condition using a proven system.

Eric Miller has been in the financial planning industry for over 20 years. He’s a co-owner of Econologics Financial Advisors – awarded an Inc. 5000 honoree for 2019. As the Chief Financial Advisor for the firm, Eric has had the good fortune to have over 10,000 financial conversations with private practice owners in various healthcare industry and helped guide them into a more optimum financial condition using a proven system.

Love the show? Subscribe, rate, review, and share!

- ptoclub.test

- Physical Therapy Owners Club Facebook

- Physical Therapy Owners Club LinkedIn

- Physical Therapy Owners Club Twitter